Many foreign companies assume that sending employees to work in Norway is operationally straightforward. The project is won, the team is selected, travel is booked. Payroll, they assume, can be sorted out later.

In practice, deploying employees to Norway can trigger a set of Norwegian reporting, payroll, tax withholding, and documentation obligations that must be in place before the first day of work — not after the first paycheck has been issued incorrectly.

The risk is not only legal. The real operational risk is what happens inside the project: delayed payroll setup, wrong tax withholding, late or missing a-melding submissions, undocumented travel and subsistence costs, and a management team that cannot clearly see what the Norwegian assignment is actually costing them.

This article explains what foreign employers should clarify before employees start working in Norway.

Why Employee Obligations Must Be Clarified Before Work Starts

Payroll setup after an employee has already started creates avoidable risk. In Norway, employer reporting, salary processing, tax withholding, and documentation requirements apply from the point employment begins — not from the point an accounting firm is first contacted.

The consequence of late setup is not just administrative inconvenience. Late or incorrect a-melding submissions attract enforcement fines. Incorrect tax withholding creates reconciliation problems for both the employer and the employee. Missing documentation of employee costs creates problems during any audit or project profitability review.

The correct sequence is: clarify obligations, set up the payroll structure, then start the assignment — not the other way around.

Does a Foreign Employer Need to Report Employees in Norway?

The short answer is: possibly, and this should be assessed before employees start work.

Skatteetaten states that foreign employers carrying out assignments in Norway have a reporting obligation and must submit the a-melding, reporting salary, benefits, and withholding tax information for employees working in Norway. This obligation is not limited to companies that have formally established a Norwegian entity.

Whether an obligation exists in a specific situation depends on factors including the nature of the work, the duration of the assignment, the tax treaty position between Norway and the employer’s home country, and the individual circumstances of the employees involved. These factors should be assessed early — ideally before the project contract is signed.

We are an accounting firm, not a law firm. We can help you understand the accounting and reporting side of these obligations and will coordinate with relevant specialists for questions that extend into tax law or employment law.

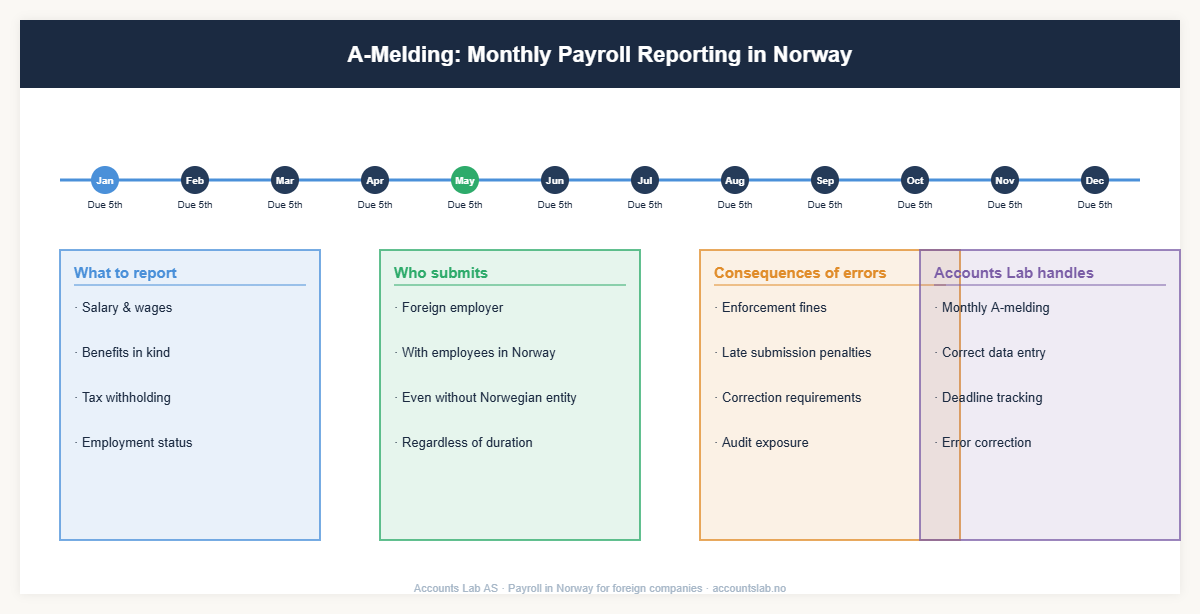

A-Melding: Monthly Reporting of Employment and Income

The A-melding is the central reporting mechanism for payroll in Norway. It is a monthly electronic report submitted by the employer that covers salary payments, benefits, tax withholding, and employment relationships.

According to Altinn, the a-melding must be submitted every month — normally by the 5th of the following month. Late or incorrect submissions can result in enforcement fines. For a foreign employer unfamiliar with Norwegian payroll systems, this deadline can easily be missed if there is no established routine.

The a-melding requires structured payroll data: correct employee identification, accurate salary figures, properly categorised benefits and allowances, and the correct withholding tax amount. Errors in any of these categories create correction work and, in some cases, direct penalties.

Skatteetaten describes the a-melding as a monthly report about income, employment, withholding tax, employer’s national insurance contributions and certain employer financial information. These employer contributions represent a significant cost on top of gross salary and should be included in the project budget before the assignment begins — not discovered after the first payroll run.

For project-based foreign companies, establishing a-melding routines before the first payroll cycle is essential. It is not something that can be set up in a week once the problem is identified.

Tax Withholding and Payroll in Norway

Employees working in Norway may become taxable in Norway on salary income earned during the assignment. Skatteetaten states that foreign employees who work in Norway will generally be liable to pay tax on salary income earned in Norway, while tax treaties between Norway and the employee’s home country may limit or modify that liability depending on individual circumstances.

For the employer, this means understanding whether withholding tax must be deducted from salary payments, at what rate, and how that withholding is reported and remitted. These questions do not have a single universal answer — they depend on tax treaty positions, the duration of work in Norway, the structure of the employer entity, and other factors. What matters from a practical standpoint is that the answers are established before salary is paid.

Norway offers a simplified tax scheme for foreign workers known as kildeskatt på lønn (PAYE). Under this scheme, employees pay a flat rate of 25% on gross salary (or 17.4% if exempt from Norwegian national insurance contributions). The scheme is available for employees earning below NOK 725,050 per year (2026). The main advantage is simplicity — tax is fully settled through the employer’s monthly withholding, and the employee does not need to file a separate tax return. Employers should assess early whether their employees qualify for the PAYE scheme or fall under the ordinary tax system (forskuddstrekk), as the administrative requirements differ significantly.

Right to Work and Foreign Employees

Before employees begin work in Norway, employers must verify that those employees have the right to work in the country. Altinn is explicit that a tax deduction card is not proof of the right to work or to live in Norway. An employer that relies on a tax card as confirmation that an employee is legally entitled to work has not fulfilled the verification obligation.

This is not an accounting matter — it is an employment and immigration matter. But it is a point that comes up regularly in the context of payroll setup, and it should be on every employer’s checklist before work starts.

Posted Workers and Documentation Requirements

Employees sent to Norway from a foreign employer — posted workers — are covered by Norwegian rules in several important areas, including working hours, health and safety, and pay conditions in sectors with generally applicable collective agreements.

Arbeidstilsynet states that employers of posted workers must ensure that documentation such as employment contracts, timesheets, and payslips are available and accessible during the posting period. For accounting purposes, this documentation connects directly to cost tracking: employee timesheets maintained for compliance purposes also provide the data needed to allocate labour costs correctly across project phases or cost centres.

Payroll Is Also Project Control

Employee costs are typically one of the largest cost drivers on a Norwegian project — particularly for service, consulting, construction, and technology assignments. If payroll is not properly set up and allocated, management cannot see with any precision what the Norwegian project is actually costing, and whether it is profitable.

Correct payroll setup means knowing which costs belong to which project, which phase, and which cost category. It means being able to reconcile what was budgeted for labour against what was actually incurred. It means having documentation for travel, subsistence, and allowances that is both compliant and useful for management reporting.

Payroll in Norway for foreign companies is not just a reporting obligation. It is a financial control function. Companies that treat it as an administrative afterthought often discover — too late — that the Norwegian assignment consumed more margin than the project budget anticipated.

Common Mistakes Foreign Employers Make in Norway

- Sending employees to Norway before clarifying payroll and reporting obligations

- Assuming that home-country payroll arrangements are sufficient for employees working in Norway

- Missing the a-melding deadline because no routine was established before work started

- Failing to document travel, subsistence, and allowances correctly from the first day

- Not verifying that employees have the right to work in Norway before they start

- Underestimating employer contributions, insurance requirements, pension questions, or social security issues

- Mixing employee costs across projects, making project profitability analysis impossible

- Contacting an accounting firm only after payroll problems have already developed

How Accounts Lab Can Help

Accounts Lab AS is a Norwegian statsautorisert regnskapsforetak — a state-authorised accounting firm. We work digitally and communicate in English, making us a practical partner for foreign companies and international management teams operating in Norway.

Accounts Lab is not built as a high-volume payroll factory. We work with a selected number of clients so we can provide close follow-up, clear communication, and proactive financial control.

- Payroll setup — establishing the correct structure before the first salary payment

- a-melding reporting — monthly submission with correct salary, benefits, and withholding data

- Employer reporting — handling Norwegian employer obligations as they apply to your situation

- Monthly payroll processing — accurate, on time, and properly documented

- Cost allocation by project — so management knows what the Norwegian assignment is actually costing

- Documentation routines — timesheets, payslips, and employment records maintained correctly

- Monthly financial reporting in English — clear visibility for your management team

- Coordination with tax and legal specialists — for questions that extend beyond accounting

For companies searching for payroll in Norway for foreign companies, the most practical first step is a short conversation to clarify what obligations apply to your specific situation — before employees start, not after.

Frequently Asked Questions

Does a foreign company always have to submit the a-melding if employees work in Norway?

Foreign employers carrying out assignments in Norway may have a reporting obligation and must often submit the a-melding. Skatteetaten’s guidance states that companies domiciled abroad carrying out assignments in Norway have a reporting obligation, but your specific situation should still be assessed before work begins.

Can we use our home-country payroll system for employees working in Norway?

Norwegian payroll reporting requirements — including the a-melding — are separate from home-country payroll systems. Even if you continue to pay employees through your existing payroll, Norwegian reporting and withholding obligations may still apply and must be handled separately.

What is the A-melding and when is it due?

The a-melding is a monthly report submitted to Norwegian authorities covering salary, benefits, tax withholding, and employment information. According to Altinn, it is normally due by the 5th of the month following the payroll period. Late submission can result in enforcement fines.

Do posted workers in Norway have the same rights as Norwegian employees?

In many respects, yes. Posted workers generally have the right to the same working conditions as Norwegian workers in the relevant sector. Employers must also maintain documentation — employment contracts, timesheets, payslips — that is accessible during the posting period.

Does Accounts Lab provide legal advice on employment or immigration matters?

No. We are an accounting firm. We handle payroll processing, a-melding reporting, employer accounting, and financial reporting. For employment law or immigration questions, we work with relevant specialists and can coordinate that input where needed.

When should we contact Accounts Lab if we are planning to send employees to Norway?

Before the project starts and before the first employee arrives. Early setup is always more efficient than correcting problems after payroll has already run incorrectly. A short initial conversation can clarify what applies to your situation and what needs to be set up before work begins.

3 Responses