Foreign contractors coming to Norway typically focus on three things: winning the contract, mobilising the team, and delivering the work on time. Reporting and documentation obligations are often treated as something to clarify later.

That is an expensive assumption. Before employees arrive on a Norwegian site, before subcontractors are engaged, and before the first invoice goes to the Norwegian client, there are reporting, payroll, and documentation requirements that may already apply.

The commercial risk extends well beyond penalties. Poor reporting setup can delay project startup, create friction with the Norwegian client, leave employees without proper payroll documentation, and produce a project cost picture that management cannot read clearly. For contractors operating on tight margins across international projects, these are real problems — not administrative formalities.

Why Contract and Employee Reporting Should Be Clarified Before Work Starts

Reporting obligations in Norway are not always obvious to foreign contractors in Norway, and they do not wait for the project to be fully mobilised. In many cases, obligations begin when the assignment starts and employees are present on Norwegian territory.

Late clarification creates practical problems: correction work with authorities, administrative pressure during active project phases, gaps in employee documentation that cannot be reconstructed after the fact, and payroll setups that were built incorrectly and need to be undone. The right approach is to assess what applies before mobilisation — not after the first reporting deadline has passed.

What Is the Assignment and Employee Register?

Norway operates an assignment and employee register — in Norwegian, oppdrags- og arbeidsforholdsregisteret — which is designed to give Norwegian tax and employment authorities visibility over foreign contractors, their employees, and their subcontractors working in Norway.

The register gives Norwegian authorities information about foreign contractors, assignments, and employees working in Norway. This information may be relevant for tax control, employer reporting, and compliance follow-up.

The reporting deadline is 14 days. Information about the assignment and any employees must be submitted via RF-1199 no later than 14 days after work in Norway has started. If changes occur — such as new employees or subcontractors being added — corrected information must be submitted within 14 days of the change. Missing this deadline can result in penalties and increased scrutiny from Norwegian tax authorities.

For foreign contractors in Norway, the register matters because it is one of the primary tools Norwegian authorities use to identify who is working where, under what contract, and whether relevant obligations have been fulfilled. The reporting form commonly associated with this system is RF-1199, administered through Skatteetaten and Altinn.

Assignments given to a foreign contractor for work in Norway or on the Norwegian continental shelf are generally reportable in the assignment and employee register. The client normally reports the assignment, while the foreign contractor reports the employees working on the assignment. The practical details should still be assessed before the project starts, especially where subcontractors, several work locations, or complex contract structures are involved.

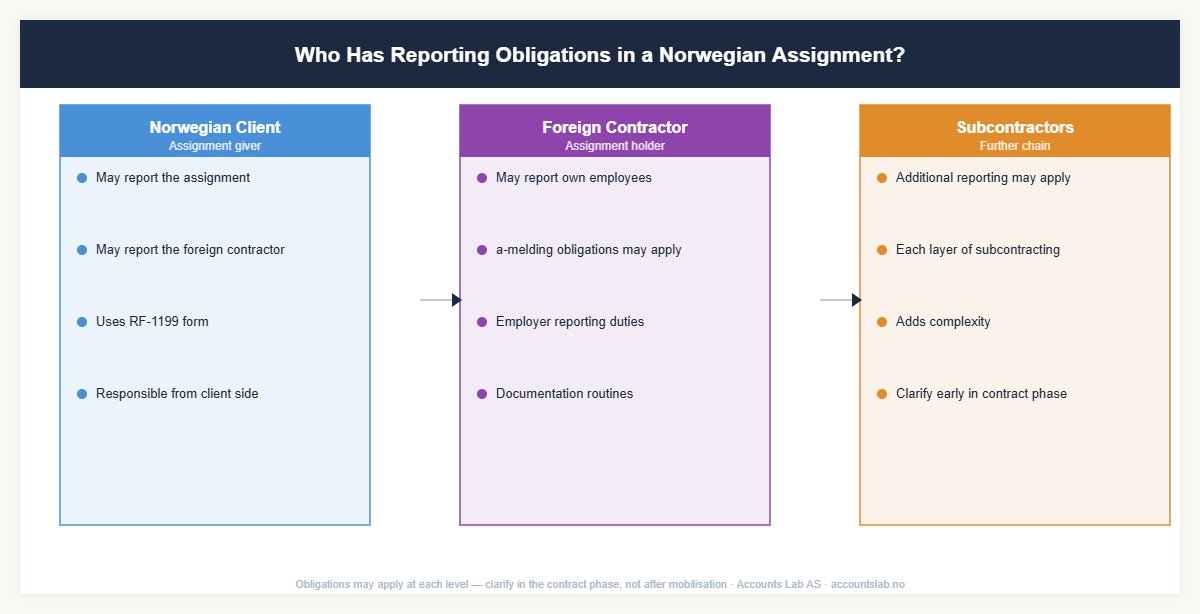

Who May Have Reporting Obligations?

The reporting picture involves several parties, and it is important to understand which obligations belong to which party.

The Norwegian client or contracting party — often referred to as the assignment giver — may have an obligation to report the assignment and the foreign contractor to Norwegian authorities. This obligation can apply when a Norwegian company engages a foreign contractor to carry out work in Norway.

The foreign contractor may have separate obligations to report employees who are working in Norway as part of the assignment. This is not the same as the client’s obligation — it is a distinct requirement that applies to the contractor directly.

Subcontractor chains make the picture more complex. When a foreign contractor engages further subcontractors, additional reporting obligations may arise at each level of the chain. Responsibilities can multiply quickly in construction, installation, and technical service projects where multiple layers of subcontracting are common.

The critical point is that these obligations should be identified and allocated clearly during the contract phase — not discovered after mobilisation has already happened.

Why Foreign Contractors Should Not Rely Only on the Norwegian Client

Even if the Norwegian client has certain reporting obligations, this does not relieve the foreign contractor of its own separate obligations. The two sets of requirements are distinct.

A foreign contractor that assumes the client will handle everything often discovers too late that its own employee reporting, payroll setup, a-melding submissions, and documentation requirements have not been addressed. The client’s reporting covers the assignment from the client’s perspective. The contractor’s obligations cover its own employees, payroll, and documentation — from the contractor’s side.

In practice, this means the foreign contractor needs its own internal routines for collecting employee data, maintaining payroll records, reporting employment relationships, and documenting work performed — regardless of what the Norwegian client is doing on its side.

How Contract Reporting Connects to Payroll and the A-Melding

Employee reporting, payroll, and the a-melding are closely connected in practice, even though they are technically separate obligations.

A foreign contractor in Norway that sends employees to work on a Norwegian project may need to submit the a-melding — the monthly electronic payroll report covering salary, benefits, tax withholding, employer’s national insurance contributions, and employment information. Getting this data organised correctly from the start — rather than reconstructing it at month-end — is a basic operational requirement.

For project accounting in Norway, this data is also the foundation for labour cost allocation. Without correct employee data flowing into payroll records from the beginning, management cannot see what the Norwegian project is actually costing in labour terms.

Subcontractors and Project Documentation

Foreign companies that use subcontractors in Norway should maintain clear and structured documentation of the entire subcontractor relationship: the contract, the scope of work, invoices, time records, employee presence on site, and cost allocation.

Poor subcontractor documentation creates cascading problems. It weakens the audit trail for tax purposes. It creates VAT issues when documentation does not clearly support the invoiced work. It makes margin analysis difficult because costs cannot be cleanly allocated to the project. And it creates problems if Norwegian authorities review the assignment and find that the contractor cannot demonstrate who was working, doing what, and when.

Project Accounting and Financial Control

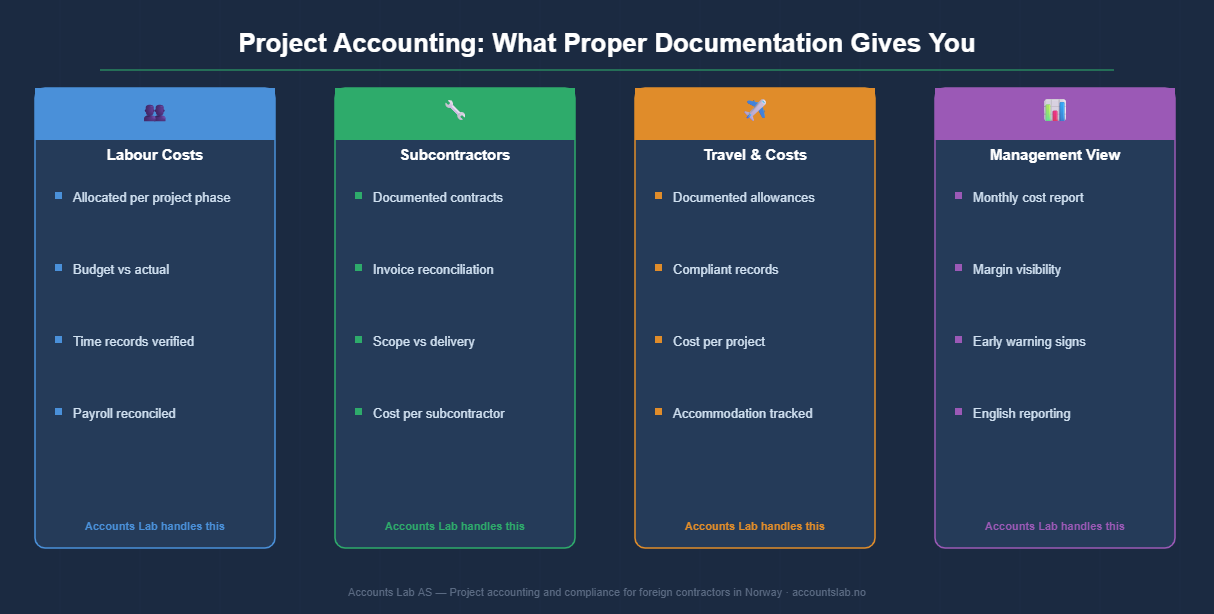

Proper contract and employee reporting is not only a compliance matter. It is also the foundation for project financial control.

When employee time is recorded correctly, subcontractor costs are allocated clearly, travel and accommodation costs are documented, and project phases are properly distinguished, management can see the true cost of the Norwegian assignment at any point. Without structured project accounting in Norway:

- Labour costs cannot be reliably allocated across project phases

- Subcontractor invoices cannot be reconciled against contracted scope

- Travel, subsistence, and equipment costs blend into general overhead

- Management sees revenue and assumes profitability — until the final cost reconciliation tells a different story

Good project accounting turns the compliance documentation into a management tool. The same timesheet that satisfies Arbeidstilsynet documentation requirements also feeds the labour cost report that tells management whether the project is on budget.

What Information Should Be Ready Before Mobilisation?

Getting organised before the project starts is the single most effective way to avoid reporting problems, payroll errors, and documentation gaps later. Before mobilisation, the following information should be collected and confirmed:

- Contracting parties and their organisation numbers or registration details

- Project location and expected duration of the assignment

- Contract value and scope of work

- Employees expected to work in Norway — names, roles, and nationalities

- Start and end dates for employee presence in Norway

- Subcontractors involved and their details

- Payroll and tax withholding setup — who processes payroll and how

- Timesheet and travel documentation routines — agreed before employees arrive

Having this information ready before the project starts makes it possible to set up reporting, payroll, and documentation routines correctly from day one — rather than reconstructing information under deadline pressure later.

Common Mistakes Foreign Contractors Make in Norway

- Starting work before clarifying what contract and employee reporting obligations apply

- Assuming the Norwegian client handles all reporting — including the contractor’s own employee obligations

- Not collecting employee information before mobilisation begins

- Missing reporting deadlines because no routine was established before the project started

- Poor documentation of subcontractor work, contracts, and invoices

- Mixing project costs with general company overhead, making margin analysis impossible

- Treating payroll, VAT, and contract reporting as separate issues managed independently in different countries

- Contacting an accountant only after the project has started — or only when a problem has already appeared

- Choosing the cheapest local accounting provider rather than one with genuine experience in accounting for foreign companies in Norway

How Accounts Lab Helps Foreign Contractors in Norway

Accounts Lab AS is a Norwegian statsautorisert regnskapsforetak — a state-authorised accounting firm. We work digitally and communicate in English, making us a practical partner for foreign contractors, project companies, and international management teams who need clear, proactive accounting support in Norway.

We are not built as a high-volume bookkeeping factory. We work with a selected number of clients so we can provide close follow-up, clear communication, and proactive financial control throughout the project lifecycle.

- Initial assessment of accounting, payroll, VAT, and reporting obligations before the project starts

- Coordination of contract and employee reporting information — understanding what needs to be reported and by whom

- Payroll setup and monthly processing — correct structure from the first payment

- A-melding routines — monthly submission with accurate data, on time

- VAT registration and bookkeeping setup — compliant from day one

- Subcontractor and project cost documentation — structured for both compliance and management use

- Monthly project financial reporting in English — so your management team can see the real cost position at any point

- Deadline management — clear routines to reduce the risk of missed reporting deadlines and enforcement fines

- Coordination with tax and legal specialists — for questions requiring legal or tax treaty interpretation beyond the accounting scope

- CFO-light financial follow-up — proactive advisory for project companies that need more than a monthly bookkeeping summary

We are an accounting firm, not a law firm. We handle the accounting, payroll, documentation, and financial reporting side. Where legal or tax interpretation is needed, we coordinate with qualified specialists.

Before you mobilise employees, subcontractors, or equipment to Norway, talk to Accounts Lab. A short clarification before project start can prevent reporting problems, payroll errors, delayed invoicing, and unclear project costs later.

Contact Accounts Lab before your project starts →

Frequently Asked Questions

Do foreign contractors in Norway need to report assignments?

This depends on the situation. Norwegian authorities operate an assignment and employee register, and reporting obligations may apply to the Norwegian client, the foreign contractor, or both — depending on the contract structure, the nature of the work, and the parties involved. Obligations should be assessed before the assignment begins, not after mobilisation.

Who reports the assignment — the Norwegian client or the foreign contractor?

For assignments given to a foreign contractor for work in Norway or on the Norwegian continental shelf, the client normally reports the assignment. The foreign contractor reports the employees working on the assignment. In subcontractor chains, the reporting picture should be clarified before work begins.

Do employees working in Norway need to be reported separately from the assignment?

Yes, in many cases. Employee reporting — including payroll, a-melding submissions, and potentially registration with Norwegian authorities — may apply separately from, and in addition to, any assignment reporting by the Norwegian client. The two sets of obligations should not be confused or assumed to be covered by the same process.

Is contract reporting the same as payroll reporting?

No. Contract and assignment reporting covers the existence and structure of the assignment relationship between the Norwegian client and the foreign contractor. Payroll reporting — through the a-melding — covers salary, benefits, tax withholding, and employer contributions for employees working in Norway. Both may apply to a foreign contractor, but they are managed through different processes.

Can Accounts Lab help with a-melding and payroll for foreign employees in Norway?

Yes. We set up payroll routines, handle monthly a-melding submissions, and manage employer reporting for foreign companies with employees working in Norway. All reporting and communication is handled in English.

Does Accounts Lab provide legal advice on contract reporting or employment obligations?

No. We are an accounting firm. We handle the accounting, payroll, and documentation side. For legal questions about reporting obligations, contract structure, or employment law, we coordinate with qualified specialists and can bring that input into the overall support picture.

2 Responses